Many people tend not to think about the importance – and potential cost – of care and support services, not until they or their loved ones need them. So it shouldn’t come as a surprise that most people don’t realise that, unlike health, care is not free. And if they are unlucky enough to have a high level of need, they could lose nearly everything they have worked hard for to meet the cost.

That is why we are reforming the care and support system and consulting on the best way to implement the changes for the benefit of all. From April 2016, we will introduce a cap on care costs and we are increasing the level of assets you can hold when means tested support becomes available. We are currently consulting on the detail of how these changes will work. But in previous and ongoing conversations about the reforms with people around the country, one thing has become clear, many are confused about how the increased help with care costs will work in practice

The charging rules for care and support are complex, but in a nutshell: at the moment, if a person has more than £23,250 of assets, so things like savings and property, they – as service users – pay for all non NHS delivered care. Below that, means tested help is available from their local council. The reforms will increase the threshold for financial help meaning more people will receive means tested support. The question then is how? To work this out, a simple but critical question must be asked:

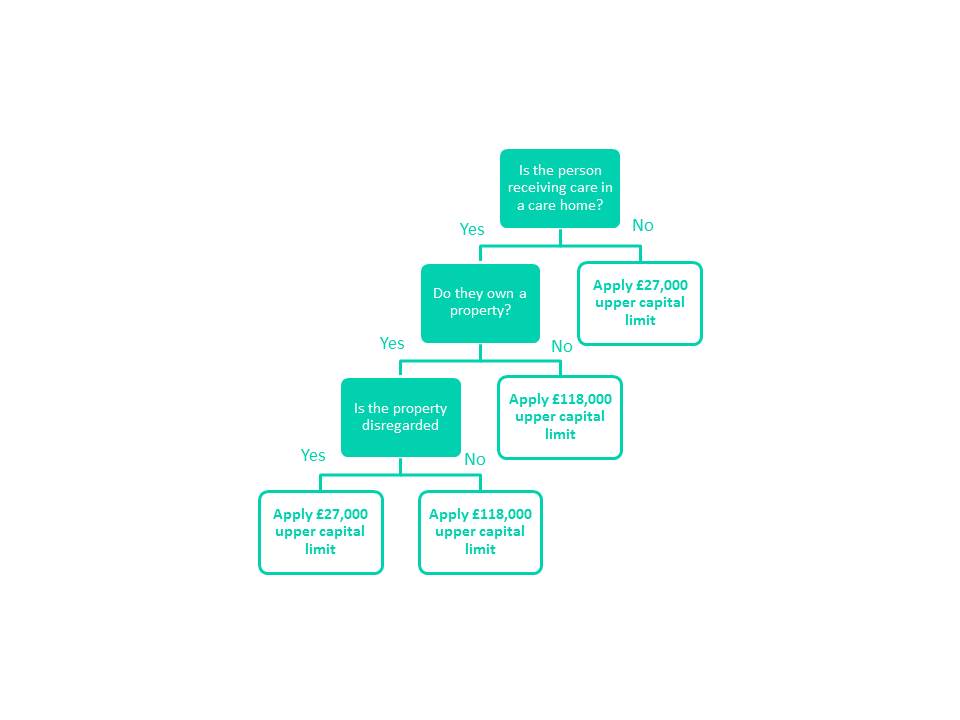

Where does a person currently receive their care?

If the answer is not in a care home, a person’s own home for example, help may become available when their assets fall below £27,000. This small increase in the costs a person is expected to cover is as often people own their own home and its value isn’t included in working out what they can afford to pay towards the cost of their care.

If, on the other hand, care is received in a care home, in many cases help may be provided when that person’s assets fall below £118,000. This includes those individuals who do not own a home. However, in some cases, where a spouse or partner is still living at home, the value of the property is not considered. In this case, help may become available when other assets fall below £27,000 because the value of the dwelling is worth much more.

In summary then, for most people living in care homes, help may be available when their assets fall below £118,000 whether they own a property or not. And if they’re living at home and receiving care, help may start at £27,000.

Click here for a visualisation of how support decisions will be made

We believe these reforms are the best way to protect people from catastrophic costs, but we need your help to make sure local authorities have the best guidance to assess and support people fairly and efficiently.

Is this the right approach? Are people sufficiently protected from losing almost everything they have? What about those who receive care at home but do not own their property? Get involved. These reforms will help set the framework for how we pay for care for the next generation.

Deadline for contributions is 30 March so make sure you have your say at www.careact2016.dh.gov.uk

4 comments

Comment by Kathryn Thomas posted on

Some paragraphs refer to £118,000 as the value of assets ie a theshold amount. If a person has less than this, financial help may be available (irrespective of how much the person has already paid themselves).

However, the paragraph beginning 'in summary' refes to £118,000 as the amount of costs which a person would have to pay before financial help may be available (irrespective of the total value of their remaining assets). This is very confusing.

If I am fortunate enough to have sufficient funds, do I pay for my own care until I have paid £118k or until my total assets fall below £118k?

Comment by Deborah Seabrook posted on

How very confusing. The article implies the amount of personal contribution is the same as the assets threshold of £27k. Please clarify.

Comment by Simon Dalziel posted on

Can we please rewrite this in English! If this is supposed to make things clearer it has not. I understand it but it is not clear to most people that the value of their home is not considered when assessing the current £23250 or future £27000.

Comment by Sara Mason posted on

Kathryn, Deborah, Simon,

You are all absolutely right. I can only apologise that an error crept in during the editing process. We have now amended the blog. thanks for pointing this out.

Sara